A seller in Secunderabad lists a used gaming laptop on a classifieds platform. The listing goes up on Friday evening. By Saturday morning, a buyer messages no questions about condition, no request to inspect, just “I want it, what is your UPI?”

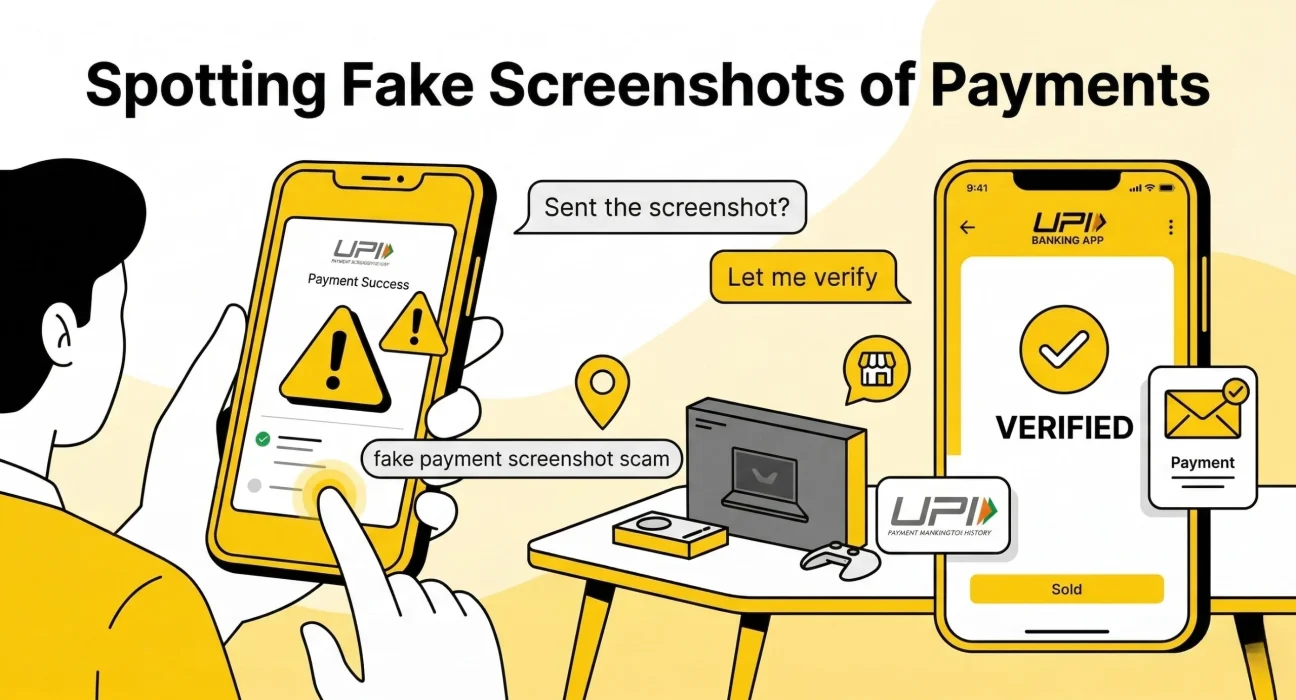

The seller shares the UPI ID. Minutes later, a screenshot arrives on WhatsApp. PhonePe interface. Green tick. Transaction ID. The correct amount. The seller’s own name as the recipient.

It looks real. It looks exactly like every genuine payment they have received before.

The buyer says: “Please confirm, my brother is nearby, he will collect it in 20 minutes.”

The seller, not wanting to lose the deal, says okay.

The brother comes. The laptop goes.

The seller opens PhonePe. No credit. No transaction. No record of any payment at all.

The screenshot was fabricated. The transaction ID was invented. The green tick meant nothing.

This scam is not rare. It happens across Hyderabad and every other Indian city, every week, to sellers who are new to online transactions and to experienced sellers who let their guard down for a moment.

The protection is simple, but only if you know it before it happens to you. Platforms like Sympl, which connect local buyers and sellers for in-person transactions, face-to-face exchange that makes this fraud structurally impossible. Among the best classified sites in Hyderabad, the safest transactions are the ones where payment is verified in person, in real time, by the seller themselves.

The Core Problem: A Screenshot Is a Photo, Not a Payment

This is the single most important thing any seller needs to understand before listing an item online in India.

A UPI payment confirmation screenshot from GPay, PhonePe, Paytm, BHIM, or any other app is an image. Images can be edited. They can be created from scratch. There are free tools available online that generate fake UPI confirmation screenshots that are visually indistinguishable from real ones to the naked eye.

A scammer does not need any technical skill to fabricate a convincing payment screenshot. They need a phone, a free app, and two minutes.

What makes this fraud so effective is that it exploits the familiarity sellers have with genuine payment confirmations. You have received real payments before. You know what they look like. The fake is designed to match that visual memory exactly and in the moment of a sale.

Sympl recommends and experienced sellers consistently confirm that the only reliable payment verification is checking your own app directly. Not a screenshot. Not an SMS. Not a notification on your screen that someone else could have triggered using a payment request rather than a transfer. Your own UPI or bank app, your own transaction history, showing an actual credit. That is the only check that counts.

How the Fake Screenshot Scam Operates Step by Step

Understanding the script helps sellers recognise it before being caught in it.

The pattern is consistent across most cases:

- The buyer expresses immediate interest often within hours of a listing going up

- They skip the usual questions about condition, age, or reason for selling

- They agree to the price quickly sometimes even offering slightly more than the asking price

- They create urgency: “I need it today”, “Can your address, my friend is near your area”, “Just confirm and I will send payment now”

- A screenshot arrives within minutes showing a completed UPI transfer with the correct amount

- They immediately follow up with pressure: “Please confirm received”, “My driver is leaving now, is it okay to come?”

- The seller, seeing what looks like a confirmed payment, agrees and the item is collected or sent before verification happens

- The seller checks their app. Nothing is there.

Variations that use the same core deception:

- A screenshot showing a “pending” payment pending is not received, and the payment may never arrive

- A screenshot from a different app than the seller’s primary one easy to dismiss as a different bank’s interface

- An edited screenshot of a real smaller transaction with the amount changed

- A screenshot generated entirely using a fake UPI receipt tool free, quick, and visually convincing

Visual Signs That a Payment Screenshot May Be Fake

While the definitive protection is never relying on a screenshot at all, knowing what to look for adds a useful layer of awareness.

Examine these elements if you receive a payment screenshot:

- The amount field is the most commonly edited part. Look for any difference in font weight, size, or colour compared to the surrounding text. Editing software often leaves subtle but visible inconsistencies here.

- The transaction ID UPI transaction IDs follow specific formats, typically 12 digits. An ID that is unusually short, unusually long, or contains letters where numbers should be is a signal.

- The timestamp does the time shown match when the message was sent? A payment screenshot sent to you at 11:15 AM showing a transaction time of 3:00 PM has not happened yet.

- Pixelation or blur around key figures editing and saving an image multiple times often degrades quality around the edited area. Look closely at the numbers if the screenshot seems slightly compressed.

- The app interface UPI apps update their design regularly. A screenshot using an outdated interface design on a conversation happening today is worth questioning.

- Your own phone a real UPI credit, triggers a sound notification, an SMS from your bank, and an in-app notification almost immediately. If none of these arrived when the screenshot was sent, the payment was not made.

None of these checks replace the fifteen-second verification in your own app. But they help you respond calmly and confidently when something looks off.

Practical Guidance: How Sympl Users Can Transact Safely Every Time

The good news is that protecting yourself from payment fraud does not require technical knowledge, special tools, or extended caution. It requires one consistent habit applied to every transaction.

The non-negotiable rule: verify before you hand over anything.

- Open your UPI app or bank app directly PhonePe, GPay, Paytm, or your bank’s own app

- Go to transaction history

- Confirm the exact amount from the correct sender appears as credited and completed

- Only after this confirmation not before should any item change hands

Sympl approach to local transactions is built around exactly this kind of direct, verifiable exchange. When you use Sympl to connect with a nearby buyer and complete the transaction in person, you are watching the payment happen in real time not trusting a screenshot sent from a distance.

Other habits that protect sellers on every platform:

- Tell buyers upfront that you will verify payment in your app before handover genuine buyers will have no objection

- For high-value items like phones, laptops, or two-wheelers, ask the buyer to make the transfer while both of you are present and watch the credit appear on your screen

- Do not allow a third party, a “friend”, a “driver”, a “colleague” to collect an item on behalf of a buyer you have never spoken to directly. If someone else is collecting, the original buyer should confirm the arrangement by phone in your presence

- Keep your listing active on Sympl and other platforms until payment is confirmed in your app. Do not mark it as sold or hold it off the market based on a screenshot

- If a buyer becomes aggressive or impatient when you say you need to verify payment, end the conversation. A genuine buyer will wait thirty seconds for you to check your phone.

For cash transactions:

- Count the notes in front of the buyer before handing over the item

- The physical equivalent of the fake screenshot scam is the overpayment trick being handed extra cash and then asked to return change before you have checked what you received

- Count it, confirm it, then proceed

How Local Buying and Selling on Sympl Eliminates This Risk

The fake payment screenshot scam is a remote fraud. It depends on the distance the seller cannot see the buyer’s screen, so they must trust an image that the buyer sends them. Local selling through Sympl removes this distance entirely.

When you connect with a buyer through Sympl and meet them in person in a parking lot, at a building lobby, or at a cafe entrance there is no screenshot involved at all. The buyer opens their UPI app in front of you, initiates the transfer, and you watch the credit appear in your own app in real time.

This is how Sympl local transaction model works in practice. Direct buyer–seller interaction means no information gap, no dependency on images that can be fabricated, and no opportunity for the standard remote fraud script to operate.

In-person, locally verified transactions are not just more convenient than remote ones, they are structurally safer. The fraud requires a gap between payment and verification. Sympl local model closes that gap by design.

For sellers who have experienced this scam or who want to ensure they never do, using Sympl to find nearby buyers and complete transactions in person is the most straightforward protection available.

Cost and Time Benefits of Getting Payment Verification Right

Every seller who has lost an item to a fake screenshot scam knows the real cost is not just financial. It is the time spent trying to recover, the loss of trust in the process, and the reluctance to list again.

None of that needs to happen.

For sellers on Sympl and local classifieds:

- A fifteen-second payment check before handover prevents losses that are difficult or impossible to recover

- In-person transactions on Sympl close the same day with confirmed payment no waiting for transfers to clear, no following up with buyers who claim it is “processing”

- No commission deducted from your sale what is agreed is what you receive, fully and immediately

For buyers:

- Low-cost buying through Sympl and similar local platforms means paying a fair price with no platform margin added on top

- Paying in person after inspection removes all ambiguity: you see the item, you pay, you take it. Clean and complete.

- Nearby buyers and sellers on Sympl transact faster than any national platform alternative without the logistics complexity that remote transactions introduce

The habit of verifying payment before handover adds fifteen seconds to every transaction. The cost of not having this habit, even once, can be far more significant.

Who Needs This Guidance Most

First-time sellers listing a phone, laptop, or household item for the first time the fake screenshot scam specifically targets people who have not encountered it before. Knowing that a screenshot is not proof of payment before your first listing is the most valuable information this blog can provide.

Students selling electronics between semesters or to fund a new purchase phones and laptops are the most targeted categories because they are portable, high-value, and easy for a scammer’s contact to collect quickly. Using Sympl for local in-person transactions eliminates this risk.

Working professionals selling premium gadgets, cameras, or two-wheelers significant amounts are involved and scammers know it. Watching the payment arrive on your screen during the meeting is worth the extra thirty seconds.

Families clearing out appliances or electronics during a home reorganisation often manage multiple buyers simultaneously and sometimes under time pressure. The payment verification habit should apply to every transaction, regardless of how genuine the buyer seems.

Anyone who receives a buyer with no questions, no negotiation, and a request for immediate collection this is the profile of a scam attempt in the majority of cases. The screenshot that follows is almost certainly fake. Recognising the pattern early is half the protection.

Conclusion:

The fake payment screenshot fraud is not technically sophisticated. It works because sellers mistake a picture for a fact.

A screenshot of a payment confirmation is an image. Images can be created and edited by anyone. The only confirmation that matters is the one visible in your own UPI or bank app, in your own transaction history, showing a completed credit.

Checking your app before handing over any item of value every time, without exception is the complete defence against this fraud. It takes fifteen seconds. It costs nothing. And it does not require any distrust of the majority of genuine buyers who complete honest transactions through Sympl and other local platforms every day.

Sympl is built around the principle of local, direct, in-person transactions where buyer and seller are present together and payment is made and confirmed in real time. This model removes the conditions the scam depends on.

The local second-hand market in Hyderabad is active, practical, and full of people completing genuine transactions without any complications. Staying safe within it is straightforward: verify before you hand over, use local platforms like Sympl that keep transactions face to face, and trust the process once payment is confirmed in your own app.

One habit. Every time. That is all it takes.